By Caroline Ennis

I. NAFTA’s Chapter 11 in Context

When the U.S. and Canada entered a free trade agreement (“FTA”) in 1989, concerns emerged over the U.S. solidifying power over Canada. The primary concern was that a “hub and spoke” model, featuring the U.S. as the hub under separate bilateral agreements with Canada and Mexico, would threaten Mexican-Canadian economic sovereignty. Thus, Canada asked Mexico to join trade negotiations, and the North American Free Trade Agreement (“NAFTA”) was born.

Bilateral investment treaties (“BITs”) are the traditional form of governance for foreign investment relations. However, NAFTA heralded in a new era of FTAs that included investment protection through investor-state dispute settlement (“ISDS”) mechanisms. NAFTA Chapter 11 aimed to protect North American investors against government mistreatment, and its ISDS provisions were intended to bolster investment in the region and benefit all parties.

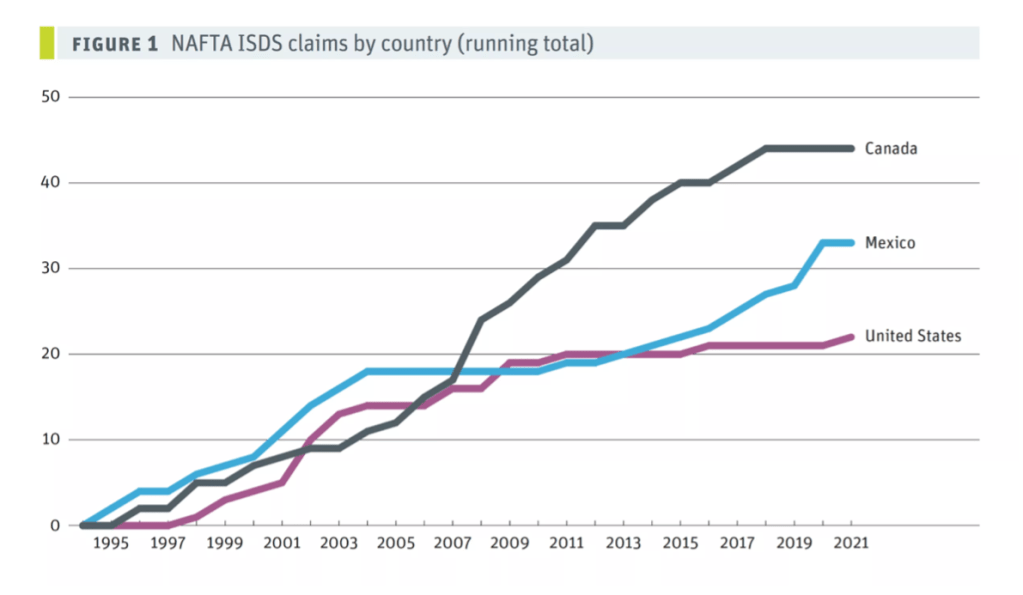

Between Chapter 11’s 1994 implementation and NAFTA’s replacement by the United States-Mexico-Canada Agreement (“USMCA”) in July 2020, NAFTA members filed ninety-nine ISDS arbitrations against each other. Nonetheless, NAFTA’s revolutionary placement of an investment chapter within an FTA still enhanced trade among its members. Meg Kinnear, who served as ICSID Secretary-General from 2009-2024, noted that because of NAFTA, many countries began using similar ISDS models. There are now over four-hundred FTAs that include an ISDS chapter, and these FTA disputes comprise about half of ICSID’s caseload.

USMCA Chapter 14 looks strikingly different from NAFTA Chapter 11. Namely, Canada is not a party to Chapter 14, which means no ISDS proceedings against Canada are allowed after July 1, 2020. However, the option to initiate legacy ISDS proceedings against Canada remained in effect until July 1, 2023 (a “legacy investment” is an investment made between January 1, 1994, and July 1, 2020). Additionally, an investor may only submit a claim for arbitration under the transition provisions in Annex 14-C, Annex 14-D, and Annex 15-E. Furthermore, USMCA requires investors to bring cases before a “competent court” of the host State for alleged treaty violations before commencing arbitration. Then, investors are required to obtain a final judgment from a local court or prove that they are unable to obtain a final judgment after thirty months of local proceedings.

I. The Sunset Scramble: Legacy Claims and Jurisdiction Questions

With the changes in Chapter 14 of the USMCA, the North American arbitration landscape changed drastically. USMCA required legacy claims to serve the host State with a notice of intent at least ninety days before commencing arbitration proceedings, and six months before for expropriation claims related to taxation measures. With the sunset period’s closing, ICSID’s NAFTA-based caseload increased sharply in FY2023; NAFTA and USMCA together accounted for twelve percent of all newly registered cases, up from four percent in the year prior. Mexico had the most cases filed against it, as five of the six ICSID cases registered in FY2023 involving North American defendants named Mexico as the respondent. Energy and mining disputes predominated in these cases.

The most high-profile case during the sunset period was TC Energy’s $15 billion claim against the U.S. over the Biden administration’s cancellation of the Keystone XL pipeline permit. TC Energy’s claim failed on jurisdictional grounds, with the tribunal ruling that the legacy provisions only permitted claims for alleged breaches that occurred while NAFTA was still in force. Thus, Biden’s January 2021 revocation, after USMCA became effective, fell outside that window.

II. Elected Judges, Exhausted Remedies: Mexico’s 2024 Judicial Reform and Investor Trap

On September 15, 2024, Mexico promulgated a sweeping constitutional overhaul of its judicial branch. Most significantly, the law mandated the removal of all sitting judges and their replacement through popular elections. The law also reduced the number of Supreme Court Justices from eleven to nine, introduced “faceless” judges for organized crime cases, and dissolved the Federal Judiciary Council. President Andrés Manuel López Obrador framed the legislation as a democratizing anti-corruption measure. On the other hand, critics saw it as a political capture of the one branch of government his party did not control.

As a result of the Mexican reforms, a potentially acute problem arises for investors. Given USMCA Chapter 14’s mandatory local litigation requirement (which did not exist under NAFTA), investors in all but a few covered sectors now must navigate Mexico’s domestic court system before seeking arbitration proceedings under the USMCA. The reforms may narrow the judiciary’s scope of intervention for investors in multiple ways: elected judges subject to popular sentiment may be less willing to suspend unconstitutional laws through the amparo process, judicial sanctions imposed by the newly elected Judicial Discipline Tribunal could chill decision-making, and the erosion of judicial powers could reduce the tools available to parties challenging State action.

“The 2026 review will determine whether USMCA’s dispute settlement architecture functions as enforceable law or elaborate fiction, and the result will impact the future predictability of North American ISDS.”

Caroline Ennis

III. 2026: What Investors Should Be Watching

The July 2026 joint review of USMCA is the most consequential moment for North American investment law since USMCA entered into force. Under the USMCA, all three parties must agree during the review on whether to extend the agreement for another sixteen-year term. Failure to reach consensus regarding whether the USMCA should stay in force would trigger mandatory annual reviews until agreement is reached or the agreement expires in 2036. For investors, each month of structural uncertainty and unresolved ambiguity threatens competitiveness, job creation, and trust in the region’s economic governance. Therefore, the Chapter 14 ISDS structure will likely be central to the joint review negotiations.

Voices in Washington are pushing for the termination of U.S.-Mexico ISDS. In March 2026, twenty-two Democratic Senators signed a letter to USTR that urged it to eliminate ISDS from the renegotiated agreement. The letter also argued that ISDS grants foreign corporations special extra-judicial rights not available to domestic companies. Investors in covered sectors, energy, telecommunications, and infrastructure should closely monitor whether the review expands, contracts, or reaffirms the narrow ISDS window that is currently in effect.

The 2026 review will determine whether USMCA’s dispute settlement architecture functions as enforceable law or elaborate fiction, and the result will impact the future predictability of North American ISDS.